Recommendation

I recommend taking a long position in Tableau Software Inc.

(DATA-NYSE), a developer of software products for business intelligence

applications, which currently trades at $92.26 per share, because it is significantly

undervalued.

The Company continues to experience

rapid growth both domestically and internationally. The revenues continue to

increase both on a YoY and a QoQ basis and the Company has been able to both

maintain and increase its customer base.

Company has been making conscious efforts towards its R&D and

continues to innovate. It recently released the latest version of its software,

Tableau 9.0, which offers advances in the areas

of visual analytics, performance, scalability, data preparation, and enterprise

capabilities.

Key investment risks include the

inability to sustain high growth rate and increased competition from other software

companies.

Company Background

The company makes software products

for business intelligence applications. It currently makes four key

products: Tableau Desktop, a self-service, powerful analytics product for

anyone with data; Tableau Server, a business intelligence platform for

organizations; Tableau Online, a cloud-based hosted version of Tableau Server;

and Tableau Public, a free cloud-based platform for analyzing and sharing

public data.

The company has

released nine major versions of its software, each

expanding and improving its products' capabilities and recently released

Tableau 9.0, which offers advances in the areas of visual analytics,

performance, scalability, data preparation, and enterprise capabilities. In

addition, Tableau Server and Tableau Online have been re-designed to deliver a

faster, more scalable, and extensible platform for customers.

Company’s products are

used by people of diverse skill levels across all kinds of organizations,

including Fortune 500 corporations, small and medium-sized businesses,

government agencies, universities, research institutions, and non-profits. As

of June 30, 2015, Company had over 32,000 customer accounts located in

over 150 different countries.

Company’s distribution

strategy is based on a "land and expand" business model and is

designed to capitalize on the ease of use, low up-front cost and collaborative

capabilities of software. To facilitate rapid adoption of it’s products,

Company provides fully-functional free trial versions of its products on its

website and has created a simple pricing model. After an initial trial or

purchase, which is often made to target a specific business need at a

grassroots level within an organization, the use of its products often spreads

across departments, divisions, and geographies, via word-of-mouth, discovery of

new use cases, and its sales efforts.

Investment Thesis

I

believe the stock is underpriced due to the following reasons:

- The existing market for analytics software is underserved and the Company has a large market allowing it to substantially expand its customer base. The rapid growth experienced by Tableau as well as an increase in its overall revenue and international revenue is a testimony to this fact. The company reported an increase of 65.2% YoY for Q2, 2015 and its international revenue increased by 83% for the same period. The international revenue now accounts for 24.5% of the Company’s total revenue and international market offers many possibilities to continue the strong growth demonstrated by the company in US.

- The Company currently has 32,000 customers located in over 150 countries, which is an increase of 52.3% YoY and an increase of 8.8% QoQ. The Company is aggressively expanding its direct sales force and indirect sales channels outside the United States and currently has products that support eight languages. It signed its first seven-figure deal in Asia-Pacific and recently opened an office in Shanghai, China and Paris, France, which represents Company’s third largest market behind Great Britain and Germany.

- Company continues to invest in its R&D efforts and its ability to continue to innovate, improve functionality, and adapt to new technologies. It recently released the latest version of its software, Tableau 9.0, which offers advances in the areas of visual analytics, performance, scalability, data preparation, and enterprise capabilities. Actions like these as well as rapid release cycles for various software allows the Company to maintain its competitive position.

Underserved market, increasing

customer base, re-investment in R&D and strong ability to innovate, offer

significant upside in taking a long position in this stock.

Valuation

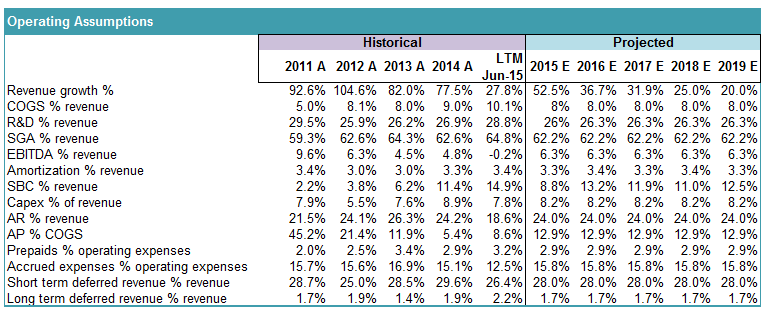

I performed a DCF calculation for

FY 2015 E to FY 2019 E using a multiples method. I made the following operating assumptions in

doing my DCF analysis:

*Please note that the projections were based on prior period actuals, information from company financials and data obtained from Bloomberg and Capital IQ.

On the basis of these operating

assumptions I made the following Cash Flow Projections:

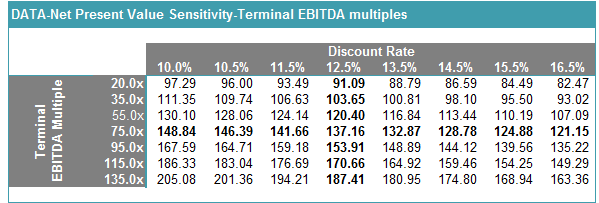

Based on the above analysis I got a

range of values. Based on the strong historical performance of the company thus

far, and its ability to innovate along with strong customer acquisitions,

improved expansion rates and increasing deal sizes, a much more conservative EBITDA

multiple should be 75.0x, which increases the valuation of the company from its

current stock price of $92.26. Additionally, a WACC rate of 12.5% is more

realistic and therefore, I believe a stock price of $137.16 is more realistic

and the company is undervalued. Even, if the company were sold at a very small

EBITDA multiple of 35.0 x (which is highly unrealistic at this point), the company’s

stock should still be trading at $103.65 using a WACC of 12.5%. Therefore, I

believe that at the very minimum the share is undervalued by 12%, although a

more realistic estimate would put the share price to be undervalued by 49%

(share price of $137.16).

Risk

factors and how to mitigate them

1.

The

company continues to aggressively grow its business. It is hiring new employees

at a rapid pace, particularly in its sales and engineering groups. Inability to

train these new employees, including its direct sales force, could negatively

impact the company’s sales as customers may loose confidence in the knowledge

and capability of its employees.

2. Company’s

sales are subject to rapidly changing technology and evolving standards. There

is competition not only from large software companies including

suppliers of traditional business intelligence products but also business

analytics software companies like Qlik, MicroStrategy, TIBCO Spotfire Inc.

Therefore, the company operates in a highly competitive environment and needs

to continue innovating and investing in its R&D. Inability to do so would negatively

impact Company’s top and bottomline.

We can mitigate these risks via put

options.